Introduction

Base Erosion and Profit Shifting (BEPS) and other international tax issues have a significant impact on India's financial market. The problems primarily arise due to profit-shifting arrangements by multinational corporations (MNCs), tax havens, and aggressive tax competition among nations. Being a developing country, India is facing a colossal revenue loss due to tax avoidance strategies followed by business groups and high-net-worth individuals. This essay presents the implications of BEPS and other international tax issues on India's financial market and suggests regulatory controls to meet such challenges.

Understanding the Issue

Global tax governance has been influenced by institutions like the Organisation for Economic Co-operation and Development (OECD) and its BEPS strategy mainly. The BEPS initiative is geared towards curbing tax avoidance by multinational enterprises using strategies like country-by-country reporting, the Common Reporting Standard (CRS), and the imposition of Pillar One and Pillar Two reforms. The strategies have been criticized as being developed-bias, with developing economies like India left behind.

India is losing substantial tax revenues as a result of profit shifting and tax competition. Reports state that corporate tax collections lost by India as a result of BEPS in 2021 totalled about 2% of total corporate tax collections. The absence of a strong global tax framework makes it easy for MNCs to take advantage of loopholes, diverting profits to low-tax destinations and eroding India's tax base.

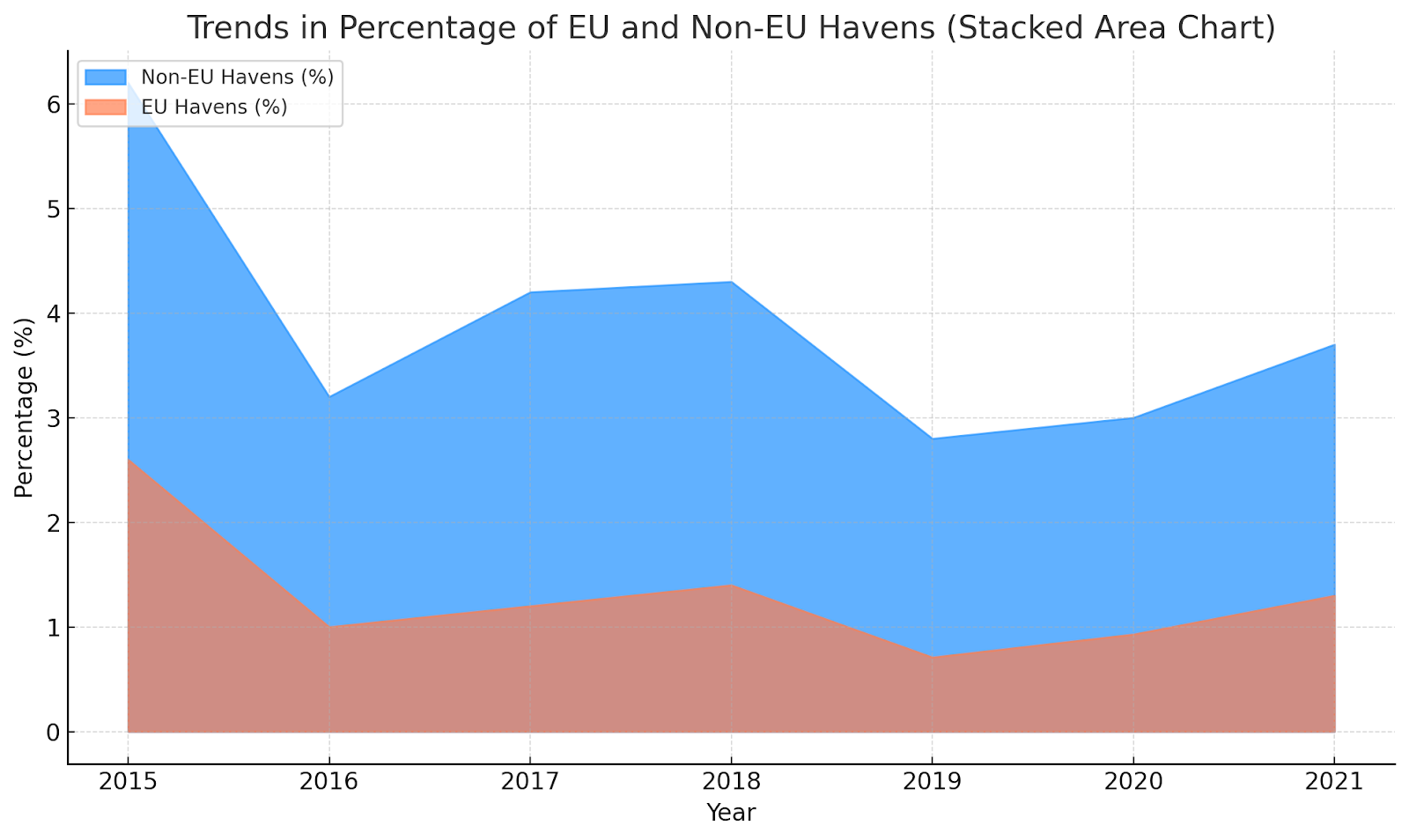

Figure 1:Trends in Corporate tax revenue lost as a share of corporate tax revenue collected (in %) and the amount of tax revenue lost in India due to profit shifting.

Note: Graphs show the trends in Corporate tax revenue lost as a share of corporate tax revenue collected (in %) and the amount of tax revenue lost in India due to profit shifting. Source: The Atlas of the Offshore World, n.d.-b

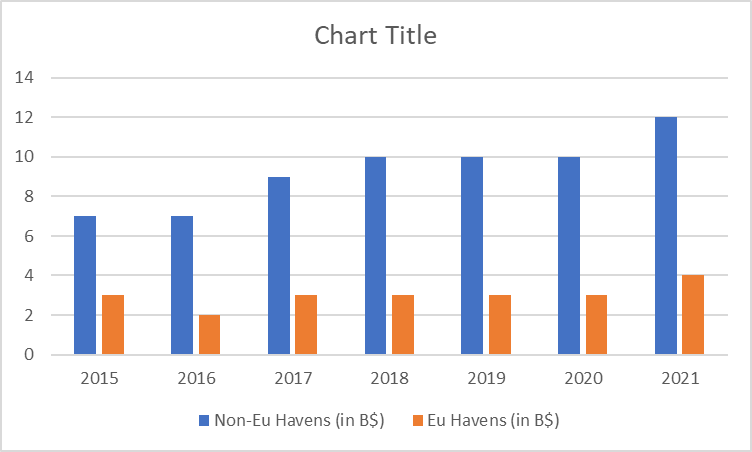

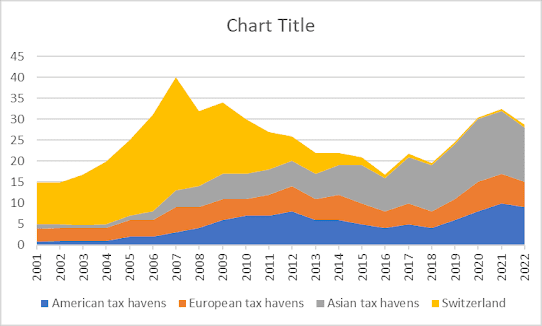

Figure 2: Trends in the cumulative amount of offshore financial wealth (equities, bonds, mutual fund shares, and associated bank deposits) held abroad by Indian households

Note: The figure shows the cumulative amount of offshore financial wealth (equities, bonds, mutual fund shares, and associated bank deposits) held abroad by Indian households. The above graph breaks down this wealth by the location of the tax haven it is held in. ( in Billion $ terms). Source: The Atlas of the Offshore World, n.d.-b

Effects on the Financial Market of India

Erosion of Public Revenue: Redistribution of profits to tax havens deprives governments of corporate tax revenues, which decreases the government's revenue. Decreased revenue constrains public investment in infrastructure, healthcare, and education, hence undermining economic growth and financial stability.

Foreign Direct Investment (FDI) Volatility: Though tax incentives are utilized for the attraction of foreign investment, harsh tax competition could lead to an unstable business atmosphere. India's reductions in its corporate tax rate to remain competitive have led to short-term peaks in investment but cannot guarantee economic sustainability in the long term.

Stock Market and Investor Confidence: The stock market responds negatively to uncertainty caused by taxes. Offshore tax leaks such as the Panama Papers and Pandora Papers have exposed the magnitude of tax evasion by Indian parties, which has eroded investor confidence. Transparency and poor regulation reduce confidence in Indian financial institutions.

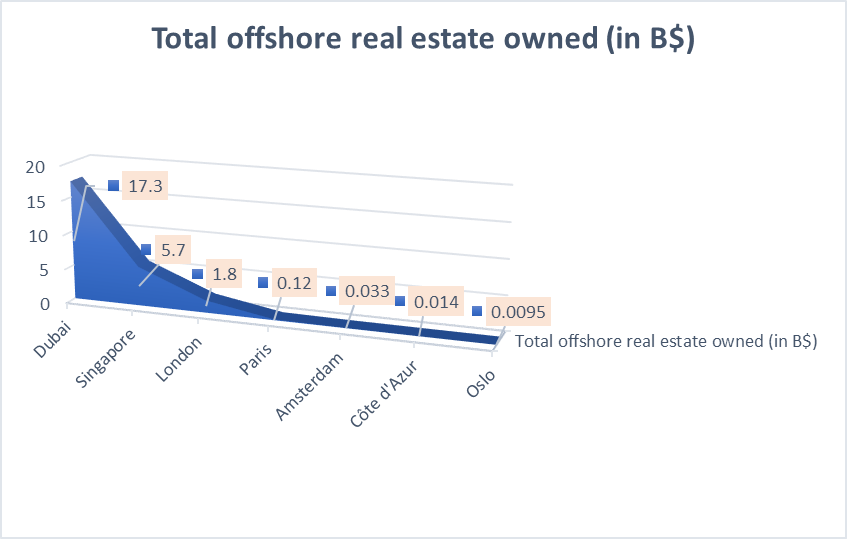

Offshore Real Estate Investment Grows: BEPS also affects capital investment as rich people and companies invest money in offshore real estate hubs such as Dubai, bypassing local investment options. This undermines the Indian banking sector by lowering local savings and capital for lending.

Figure 3: Offshore Real Estate Wealth in 6 Global Cities and Regions by Indians

Note: Graph shows Offshore real estate wealth in 6 global cities and regions by Indians. Total Offshore real estate wealth is 24.93 bn USD and it is 0.87% of the Country’s GDP. Source: The Atlas of the Offshore World, n.d.-b

Addressing BEPS and Tax Challenges

To tackle BEPS and related tax issues, India needs a multi-pronged regulatory approach, combining domestic reforms with active participation in global tax governance.

1. Enforcement of Domestic Tax Laws: India has gone on to tackle BEPS via, among others, the General Anti-Avoidance Rule (GAAR) and the reform of the Income Tax Act. There is still, however, a need to consolidate tax enforcement.

Compulsory public country-by-country reporting: Requiring MNCs to disclose detailed financial information on their operations in all countries can hold them more accountable and transparent.

Strengthening Transfer Pricing Regulations: India will have to enhance its regulation on intra-group transactions to prevent profit shifting in the form of high royalty payments and management fees.

2. Enhancing International Cooperation: The current OECD-led framework has been criticized for favoring developed nations, necessitating a more inclusive approach.

Support for a UN-Led Global Tax Policy Framework: India has supported a UN-led global tax policy framework to help ensure equitable representation of developing nations in world tax policy development.

Strengthening Automatic Exchange of Information (AEOI) and Common Reporting Standard (CRS): Better tools to enforce more effective monitoring of undeclared offshore assets can discourage tax evasion.

3. Fighting Tax Havens and Offshore Wealth

India must implement tougher policies to discourage tax evasion through offshore deposits and property investment.

Extensive Offshore Asset Disclosure Mechanisms: The government should intensify surveillance of Indian investments in tax havens and impose a penalty for nondisclosure.

Prioritizing Beneficial Ownership Transparency: Mandatory disclosure of ultimate ownership arrangements in offshore accounts will stop illicit financial flows.

4. Execution of Digital Taxation Policies

With the digital economy growing rapidly, India must adapt its tax policies to ensure fair revenue collection from multinational digital enterprises.

Strengthening Equalization Levy: Expanding the base of the equalization levy on digital services will allow India to tax revenue from digital entities without a physical presence in India.

Implementing OECD's Pillar One with Modifications: Although OECD's Pillar One aims to redistribute taxing rights, India needs to negotiate terms more suitable for developing countries.

Conclusion

The BEPS and tax competition challenges undermine India's financial stability, lowering tax revenues, deterring domestic investment, and boosting offshore financial flows. OECD-led frameworks have progressed but not to the extent of addressing the concerns of developing countries. A UN-led tax governance model can provide a more balanced solution by providing equitable representation in global tax policymaking.

India should take a balanced approach to fortifying its domestic tax policy, encouraging openness, improving taxation in the digital era, and pursuing inclusive international cooperation. Adopting these methods will enable India to protect its financial market as well as earn sustainable economic progress while mitigating the negative implications of BEPS and global tax concerns.

No comments:

Post a Comment