Fintech, or financial technology, encompasses the use of technological advancements to deliver financial services. While technology integration in banking has been evolving for decades, the recent rapid adoption of cutting-edge technologies by a substantial segment of the population is remarkable and presents significant opportunities to enhance financial inclusion in India.

The impressive growth of the fintech sector can be attributed to several key factors. These include extensive last-mile mobile connectivity (which stands at 95% according to MoSPI), the establishment of identity through Aadhar enrollment (with a staggering 138 crore enrollments to date), and the promotion of financial inclusion initiatives such as the Jan Dhan Yojana, which has seen the opening of 51 crore accounts by 2023 aimed at serving the unbanked population.

On the technological front, scalable platforms like IMPS and UPI have emerged to facilitate smoother transactions, along with the availability of UPI, GSTIN, and Digi Locker services to both banking and fintech industries. Together, these elements have fueled the rapid advancement of fintech in India.

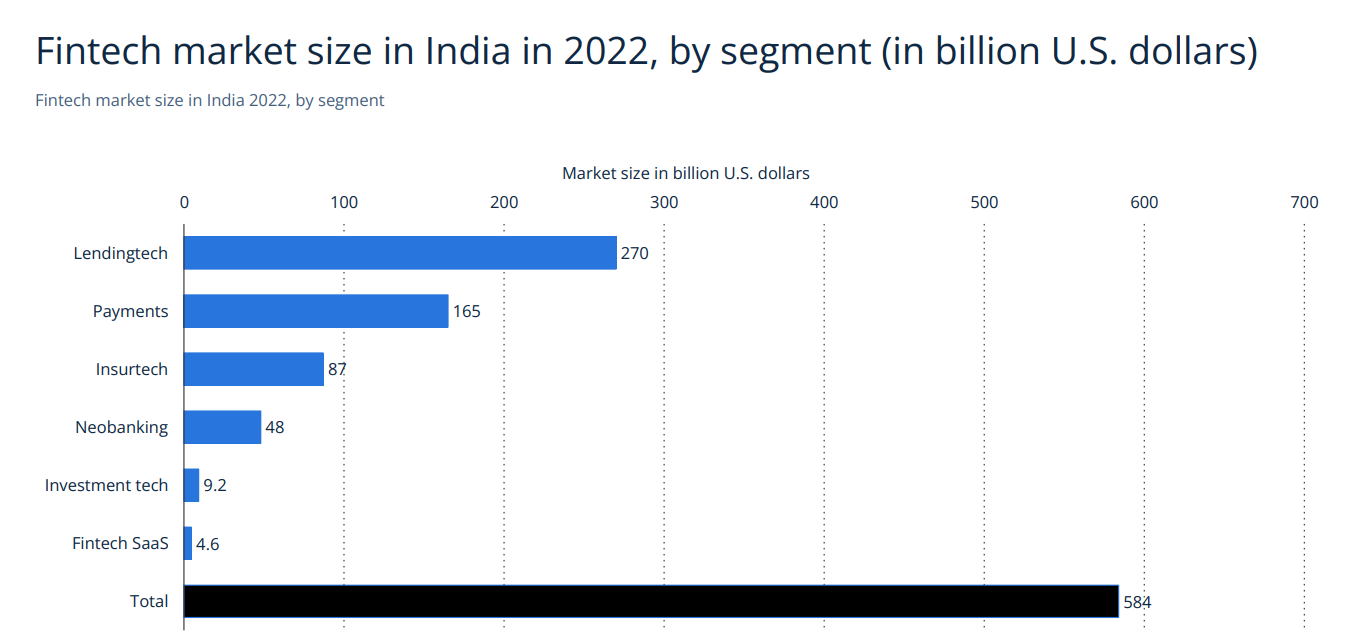

Figure: Fintech Market Size in 2022

Note: The above chart shows the sector-wise share of the Fintech market in India in 2022.

Financial technology (fintech) has become a crucial player in promoting financial inclusion in India. By utilising innovative technologies, fintech companies are bridging gaps in the traditional banking system, making financial services more accessible, affordable, and tailored to the diverse needs of the population.

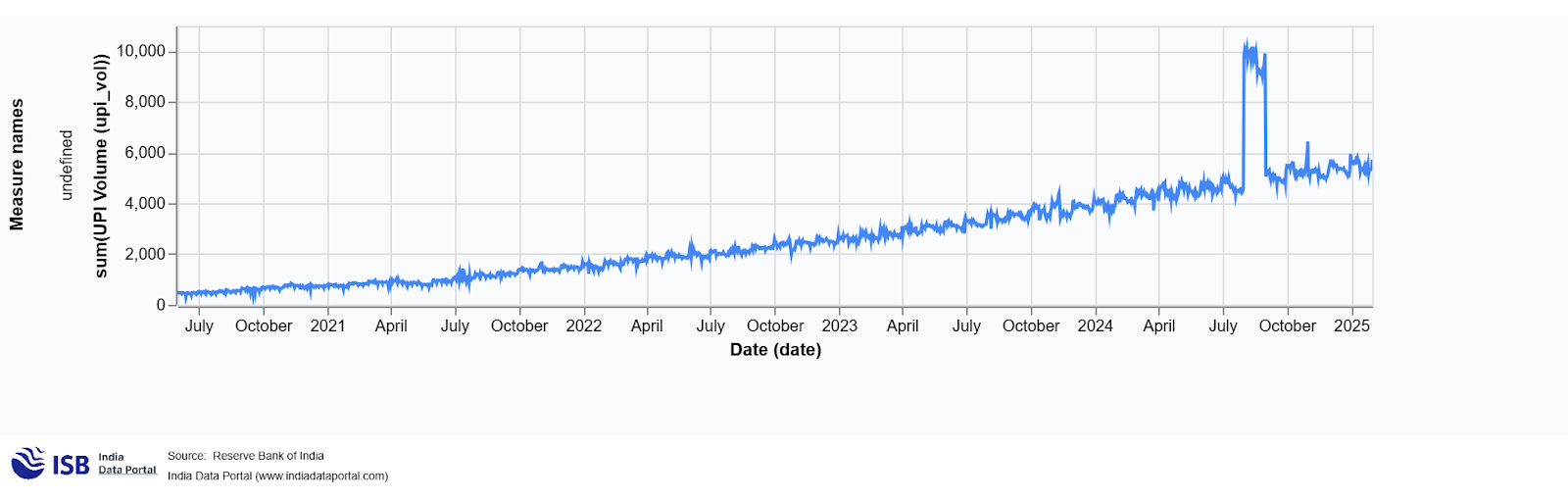

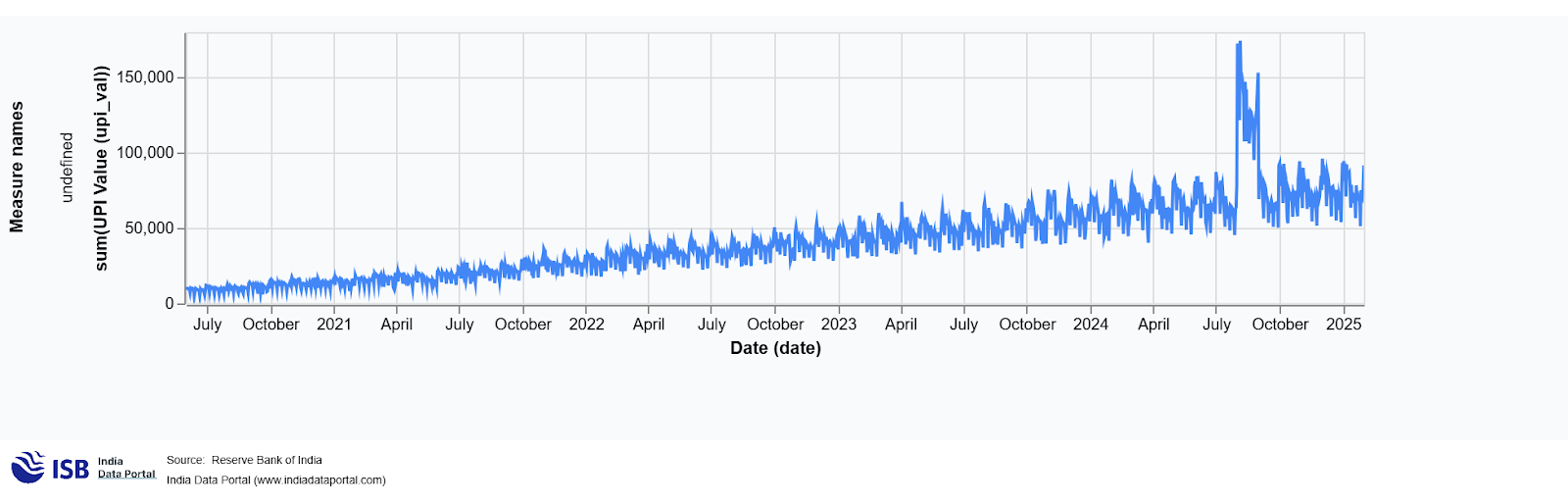

The rise of digital payment platforms has been vital in enhancing financial inclusion. The Unified Payments Interface (UPI), introduced by the National Payments Corporation of India, has transformed the payments landscape. As of January 2025, UPI accounted for 48.4% of all digital transactions in the country, boasting over 590 million registered users (Reuters, 2025). This widespread adoption indicates a shift toward a cashless economy, enabling even those in remote areas to engage in digital financial activities.

Figure: UPI volume and value between July 2020 and Jan,2025)

Note:RBI data on UPI volume and value between (July,2020) and (Jan,2025)

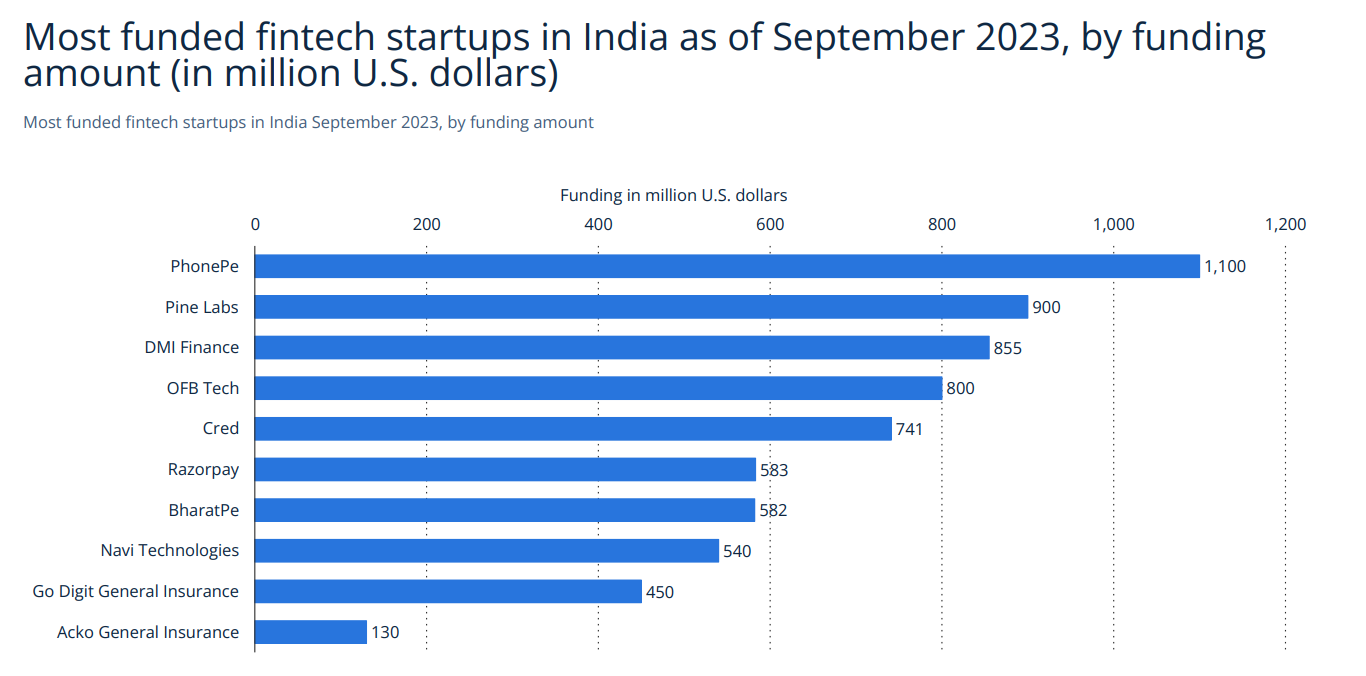

India's FinTech sector has garnered significant investment, with over USD 20 billion in funding over the past five years, which constitutes 21% of total startup funding (PwC, 2024). Foreign direct investment (FDI) and venture capital inflows have significantly contributed to the growth of financial technology solutions, particularly in digital lending and wealth management. The rise of digital lending platforms is helping to close credit gaps, especially for micro, small, and medium enterprises (MSMEs), which have historically faced challenges in accessing formal credit.

Note: Source taken from Fintech News

Fintech firms are also redefining microfinance by providing alternative lending solutions. Companies like Capital Float and CreditMantri leverage digital financial transaction data along with alternative data sources—such as value chain information and social network activity—to assess creditworthiness. This methodology allows for small loans to individuals and small businesses that lack traditional credit histories, thereby fostering entrepreneurship and economic growth.

In addressing gender disparities in financial access, fintech companies are developing products specifically designed for women. By offering user-friendly digital platforms, these firms empower women to manage their finances independently. The Reserve Bank of India's Financial Inclusion Index reflects this progress, increasing from 43.4 in 2017 to 56.4 in 2022, largely due to improved financial access for women (Asian Development Bank, 2023).

The Reserve Bank of India (RBI) has been proactive in creating a supportive environment for fintech growth. The Payments Vision 2025 document emphasises the '5 Is'—Integrity, Inclusion, Innovation, Institutionalisation, and Internationalisation—as foundational pillars for advancing payment systems. This strategic focus aims to enhance the reach and efficiency of digital payments, thereby promoting financial inclusion.

Access to credit is a crucial driver of economic growth, particularly for India's MSME sector, which contributes nearly 30% of the country's GDP. However, only 10% of small businesses have access to formal credit, highlighting ongoing challenges in financial inclusion (India-Fintech-Report, 2020).

Despite significant advancements, challenges remain. Ensuring data security, enhancing digital literacy, and extending infrastructure to rural areas are critical areas needing attention. Collaborative efforts between fintech companies, regulatory bodies, and traditional financial institutions are essential to overcome these challenges and maintain momentum toward comprehensive financial inclusion.

To tackle these issues, digital lending platforms are utilising artificial intelligence and machine learning to evaluate creditworthiness using criteria beyond traditional banking parameters. Alternatives such as supply chain financing, peer-to-peer lending, and embedded finance are gaining popularity as funding mechanisms (Investing in India’s FinTech Disruption, 2024)

In summary, fintech's innovative approaches are transforming India's financial landscape, making it more inclusive and accessible. With continuous innovation and supportive regulatory frameworks, fintech is well-positioned to play a central role in achieving the nation’s financial inclusion objectives.

No comments:

Post a Comment