India is experiencing a potential economic boom due to its demographic transition, which will result in a large proportion of the working-age population compared to the non-working population. India's median age is expected to be around 28 to 29 years between 2025 and 2030, making it one of the youngest countries in terms of demographic structure. Simon, in his influential book ‘The Ultimate Resource (1981)’, showed that rapid population growth can lead to positive impacts on economic development (Simon, 1981). However, to realise the perceived benefits, the correct policies and environment must be put in place(Bloom et al., 2003). Despite having a young population, India struggles to generate employment. The high youth unemployment rate is a significant concern, averaging about 6-7% in 2019-2020. India requires investment, skill development, and job creation to harness its large youth population for significant GDP growth(S. Bhalotra et al.,2010).

India must develop economic and social infrastructure to leverage its demographic dividend. Universal education is essential for creating a skilled workforce, enabling the country to realise this potential(Dreze et al.,2013). The National Skill Development Corporation (NSDC) predicted that by 2025, India would require an additional 109.73 million human resources across 24 critical industries. This emphasises the importance of skill development activities to capitalise on the demographic dividend. Thus, suitable vocational training and skill development programs that are suited to industrial demands are to be imparted to the youth( Agrawal, 2012). Emphasising the importance of investing in health, reproductive, maternal, and child health secures a productive and capable workforce(Bloom et al., 2010).

In India, women's labour force participation has been historically lower than men's due to gender barriers. Eliminating these obstacles could yield significant economic gains( Das Gupta et al., 2003). Different Indian states have undergone various stages of demographic transformation. Southern states like Kerala and Tamil Nadu have younger populations compared to northern states such as Uttar Pradesh and Bihar. Addressing regional imbalances is crucial since demographic profiles can impact policies(Rajan et al., 2013). Emphasis should be on governance, policy, and institutional reforms. To unlock the demographic dividend, promote labour laws, ease of doing business, and entrepreneurship(Ahuja et al., 2006).

With forecasting the fleeting nature of the demographic dividend, elder care and social security planning measures have to be undertaken with priority(Narayana,2011). Interstate migration plays a key role in India's structural transformation and economic development. People from less developed states like Bihar, Jharkhand, and Uttar Pradesh move to states like Kerala, Punjab, and Maharashtra in search of better employment and earning opportunities(Parida et al., 2020; Parida,2019).

Public spending on key sectors as a percentage of GDP shows significant deficiencies. In 2021-22, health spending was 1.84%, and education was only 2.7% in 2023-24, both falling short compared to developed countries. Infrastructure spending was allocated at 3.4%, while social security accounted for 7.8% of GDP. Overall, these levels of public spending are inadequate to address the challenges in education, health, skill development, and infrastructure in India.

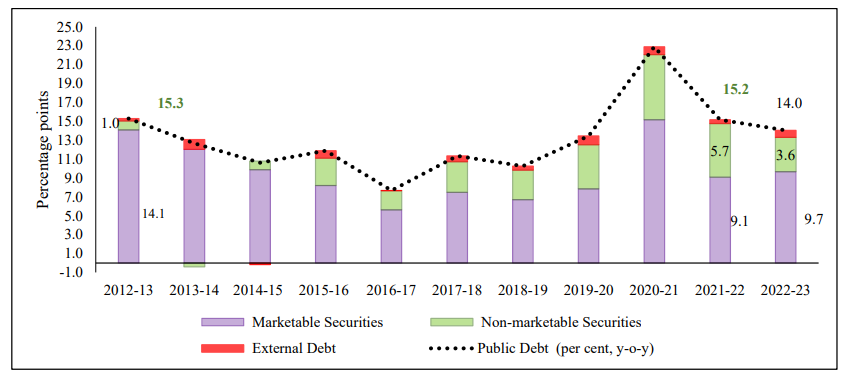

Public spending on education, health, and infrastructure is essential for leveraging India's demographic dividend for economic growth. As of March 2023, public debt stood at ₹138.2 lakh crore, or 51.3% of GDP, with 95.2% in domestic currency, indicating low currency risk. Most external debt is from official sources, minimizing market volatility. The majority of debt has fixed interest rates, with only 1.7% floating, ensuring stable interest payments. The weighted average residual maturity of dated securities was 11.9 years, with 29.1% maturing in up to 5 years, reducing medium-term rollover risk(MINISTRY OF FINANCE et al., 2022).

Chart 1: Year-on-Year growth in public debt

(Source: Status Paper on Government Debt for 2022-23 in India)

Debt management operations extend maturities and reduce risk. Commercial banks reduced their share of debt from 40.3% in March 2019 to 36.6% in March 2023, while insurance companies and provident funds hold 26.0% and 4.7%, respectively. The Government's Debt Management Strategy (DMS) assesses the debt profile, indicating low risk. (MINISTRY OF FINANCE et al., 2022).

The budgeted allocation for capital expenditure stands at a mere 3.4% of GDP(2024-25), which is significantly insufficient. Besides, Y-o-Y public debt growth is more or less the same except for the pandemic year(Chart 1). This situation necessitates increased public borrowing to adequately fund education, health, and infrastructure needs. Many authors argue that higher debt levels can promote greater growth or welfare if the funds are invested in development projects. (Ghosh, 1998; Greiner and Fincke, 2015).

The Government of India's debt management strategies allow for higher public debt, enabling investments in social and physical infrastructure to leverage demographic potential. Publicly funded infrastructure projects are more transparent and accountable, and government debt is generally cheaper than private debt, making it a cost-effective financing option.(Chong et al., 2013). Caution is needed as higher public borrowing may lead to inflation or crowding out in markets, given India's statutory debt and fiscal deficit limits.

Self-employment programs and vocational education are vital for job creation, especially for harnessing India's youthful workforce in Micro, Small & Medium Enterprises (MSMEs). Immediate agricultural reforms are essential to reduce food prices and facilitate labour shifts to industrial and service sectors. Through global remittances, India benefits significantly by reducing poverty and inequality, enhancing savings, investing in human capital, and driving economic growth through increased demand(Parida et al.,2015). To ensure a steady flow of remittances, it's vital to adopt sustainable socio-economic policies and strengthen diplomatic relations for the benefit of individuals and communities.

The Chinese growth story was driven by government initiatives, with local governments innovatively funding infrastructure through financing vehicles, without private or multilateral support. In contrast, India faces high debt and a need for resources for social services, requiring a balanced mix of public and private investment to enhance infrastructure while leveraging its demographic advantages(Chong et al., 2013).

Large infrastructure projects are still associated with the government as they involve huge upfront costs, planning and construction. Besides, investment in infrastructure causes positive externalities arising from network effects(Chong et al., 2013). To address public infrastructure financing challenges, encouraging private sector participation through public-private partnerships (PPPs) is vital. While governments value PPPs for risk management, effective structuring is necessary, and continued public support, such as viability gap funding, is essential to attract private investment(International Monetary Fund (IMF) et al., 2019).

During the 12th Five-Year Plan (2012-2017), government spending on infrastructure was 10% of GDP, with private sector contributions rising to 40%, primarily from bank loans. However, sectoral limits on bank loans restrict further exposure to infrastructure. To enhance private financing, the GOI established the India Infrastructure Finance Company Limited (IIFCL) and an infrastructure debt fund to issue bonds to long-term investors, using the proceeds to refinance bank loans for PPP projects in India, targeting insurance and pension funds for additional financing(International Monetary Fund (IMF) et al., 2019).

Reform measures are essential for sustainable PPPs in infrastructure. Over 50% of projects face delays due to regulatory hurdles, land acquisition issues, environmental clearances, and sector-specific bottlenecks, leading to cost overruns and project viability concerns. The risk-return profile of these projects affects private investment and government policy decisions. Additionally, the government could leverage a strong capital market and resources from Multilateral Development Banks to meet infrastructure funding needs (Chong et al., 2013). To attract private investments in infrastructure, the GOI should enhance service delivery, create accessible land banks, ease regulations, ensure transparency, improve dispute resolution, and offer viability gap funding. These measures will boost investor confidence and reduce project risks.

By strategically incurring public debt for infrastructure and employment, India can unlock its demographic dividend, creating a virtuous cycle of growth, job creation, and private investment.

No comments:

Post a Comment