Taxation and Mobility: A Cross-Time Analysis of India’s Experience

This article explores tax-related migration from ancient India to modern time. Tax migration refers to the effects of taxation on the geographic mobility of people. There is a rich history in ancient India of kings providing tax exemptions to encourage highly skilled artisans, poets, astrologers, and scholars to migrate and settle to promote learning, elevate cultural and religious life, and improve societal well-being in their country. Tax-free agraharas were granted to Brahmins to settle and teach in new regions, as recorded in Chola copperplate inscriptions. The Arthashastra recommends land and tax holidays to attract skilled migrants and develop frontier areas. Buddhist Sanghas were gifted entire villages free from state levies to support monastic life. Even the legend of Agastya’s southern migration reflects such royal patronage through land grants and privileges. Thus, the tax exemptions acted as a key element to encourage migration and settlement since ancient times. Does this phenomenon continue even today? Let us examine.

The research establishes the fact that tax-related migration is very common among distinguished personalities who are in the fields of invention, sports, and acting even today. What fuels this trend? Of course, there could be mutual benefits for both state and tax-migrants. It is reported that actor Akshay Kumar has obtained Non-Resident Indian (NRI) status primarily for tax purposes, allowing his global professional income to remain outside the Indian tax net. This strategy is not uncommon among high-profile individuals—such as celebrities, sportspersons, and tech entrepreneurs—who often earn substantial cross-border incomes. Among various motivations, one key reason individuals opt for Non-Resident or Non-Domiciled (Non-Dom) status is to minimize their tax burden by relocating their tax residency to countries that offer low or zero personal income tax regimes.(NRI - refers to persons who stayed abroad for more than 182 days in a year)

Further, studies found that the High-Net-Worth- Individuals(HNWI) are highly -elastic to the tax rates and readily mobile to change their resident status to save them from paying large taxes. India has increasingly witnessed this trend. Migrating the wealth to offshore havens in response to high-tax-rates is a long- existing trend. As we see several tax havens offer mechanisms to conceal wealth in their countries in the form of equities, real assets, financial instruments etc. (HNWI- refers to persons who have ₹5 crore and above in investible assets as per SEBI)

The HSBC, Panama, Paradise, Pandora, and Dubai leaks together show a clear pattern of Indians hiding wealth offshore. The HSBC Swiss leaks (2015) alone revealed over 1,000 Indian account holders with undeclared assets worth more than $4.1 billion. The Panama Papers (2016) and Paradise Papers (2017) exposed secret offshore companies linked to politicians, actors, and business groups. However, there is a worrying trend of exodus of HNWI to foreign destinations. What exactly inspires this trend?

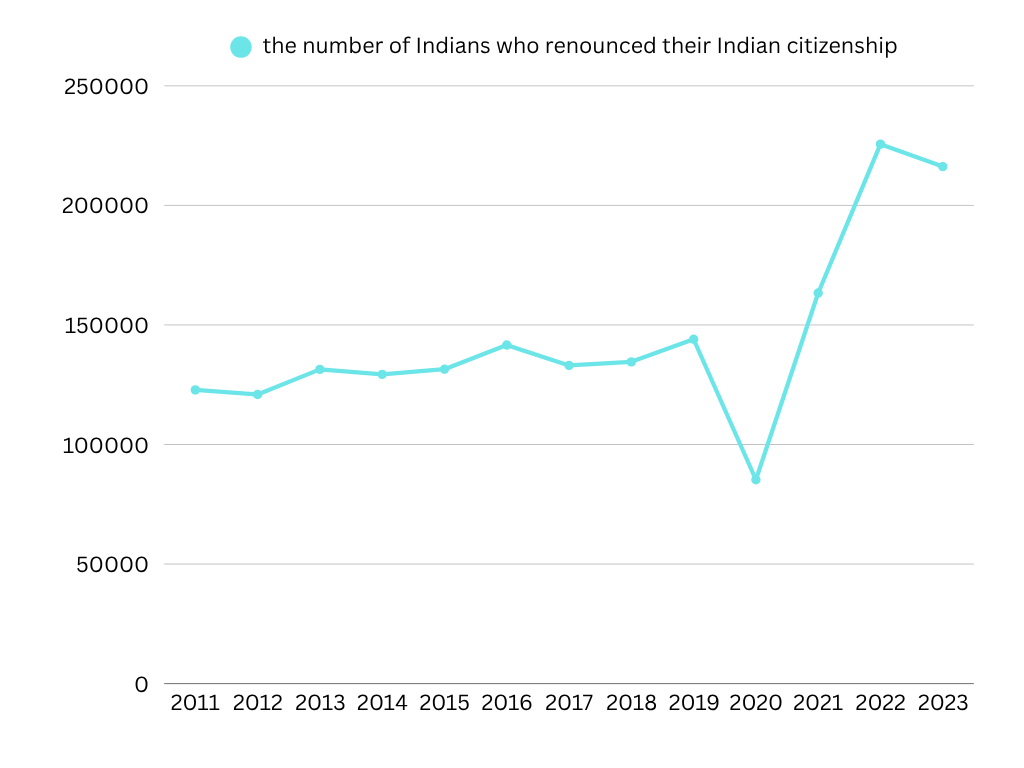

The trend analysis reveals that from 2011 to 2019, the number of people renouncing Indian citizenship remained relatively stable, ranging between 1,20,000 and 1,45,000 annually. A sharp dip occurred in 2020, with the number falling to around 85,000—likely due to COVID-19-related travel restrictions and global uncertainty. This was followed by a dramatic rise, 2021: 1,60,000, 2022: Peak at 2,25,000 (highest in the period), 2023: Slight decline to 2,15,000, but still historically high. As per the Ministry of External Affairs(MEA), reasons for renouncing citizenship are personal. Also, MEA acknowledges the potential of the global workplace in an era of a knowledge economy.

Trends in the Indians who renounced citizenship:

There could be several pull factors and push factors to this structural shift in rise in number. The push factors could be deteriorating quality of life, lack of job opportunities, lack of recognition of talent, high taxation rates( both direct and indirect). The pull factors include zero or low tax rates, better job-cum-remuneration, quality of life, career prospects, better social security etc. However, we lack data to ascertain what exactly drove them to renounce Indian citizenship.

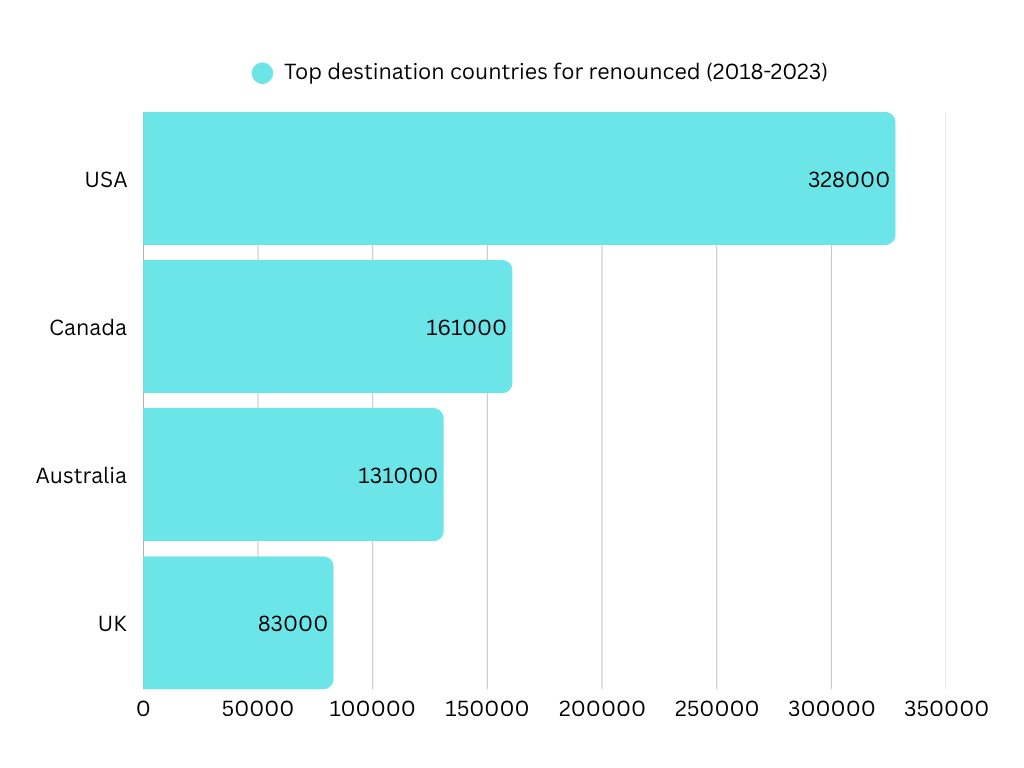

Despite the lack of direct evidence, the countries wherein these people took citizenship offers some insights about the motives. USA, Canada, and Australia accounting for the choices of more than 75% of the renounced. These patterns underscore that Indian emigrants prioritize countries with transparent immigration systems, better social infrastructure, stronger passports, and favorable work or business conditions. The dominance of the U.S. also reflects the continued demand for high-skilled Indian workers, especially in tech and healthcare sectors.

Top destination countries for renounced from India:

From the above analysis, safely, we can conclude that this trend of renouncements to anglophonic countries as “career oriented mobility” rather than tax-based-migration, as these countries do not offer any preferential taxation regime for immigrants and also tax rates are relatively high.

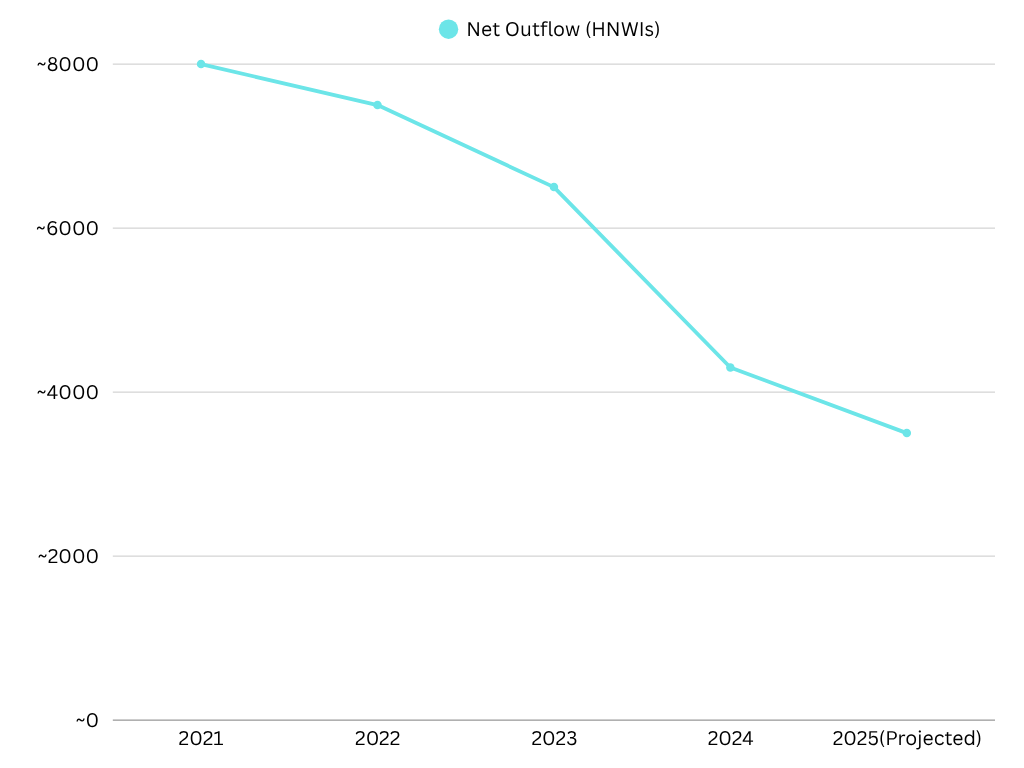

On the other hand, there was a persistent trend of exodus of HNWI in the recent past. As per the Henley & Partners Private Wealth Migration Reports (2022–2025), India is one of the top countries where exodus of HNWI persists. The figure below captures the trend of HNWI exodus from 2021 to 2025(projected). The report points to the fact that most of the HNWI emigration happens to UAE. Although the trend is not so alarming, it reveals the socio-economic preferences of the HNWI in choosing UAE, US and Singapore. Taxation is one of the major reasons driving this trend. The major reasons include UAE offers Zero personal income tax and other favourable disclosure norms. On the contrary, India tightened the disclosure norms on the global incomes of the tax residents with the Black Money Act etc.

Trends in exodus of High Net Worth Individuals from India:

According to Henley & Partners, India continues to lose large numbers of millionaires, especially to the UAE. However, in our view these outflows are not particularly concerning as India continues to produce far more new HNWIs than it loses to emigration. Furthermore, the bulk of the millionaires who leave India tend to retain business interests and second homes in the country, which is a positive sign. Though re-assuring, we cannot be complacent with the trend. Exodus of HNWI means not only loss of tax revenue, also, impact on growth of private jobs, innovation, investor confidence, business sentiment etc. India must take necessary steps to reverse this trend at the earliest.

Comparative chart of tax rates of relevant countries:

In ancient India, kings attracted talent across disciplines by offering land grants and tax-exempt revenue villages, thereby enriching societal and economic life. Drawing inspiration from this historical approach, modern India must focus on rationalizing its tax regime and simplifying compliance to retain high-net-worth individuals. Providing targeted incentives for returning NRIs and fostering investor confidence are equally important. At the same time, enforcement against offshore tax evasion should be balanced with the need to support global mobility. Broader reforms aimed at improving ease of living and doing business will be essential for sustaining long-term economic retention.

Retaining talent today requires the wisdom of ancient incentives with the agility of modern reform